Award-winning PDF software

Publication 1212 Form: What You Should Know

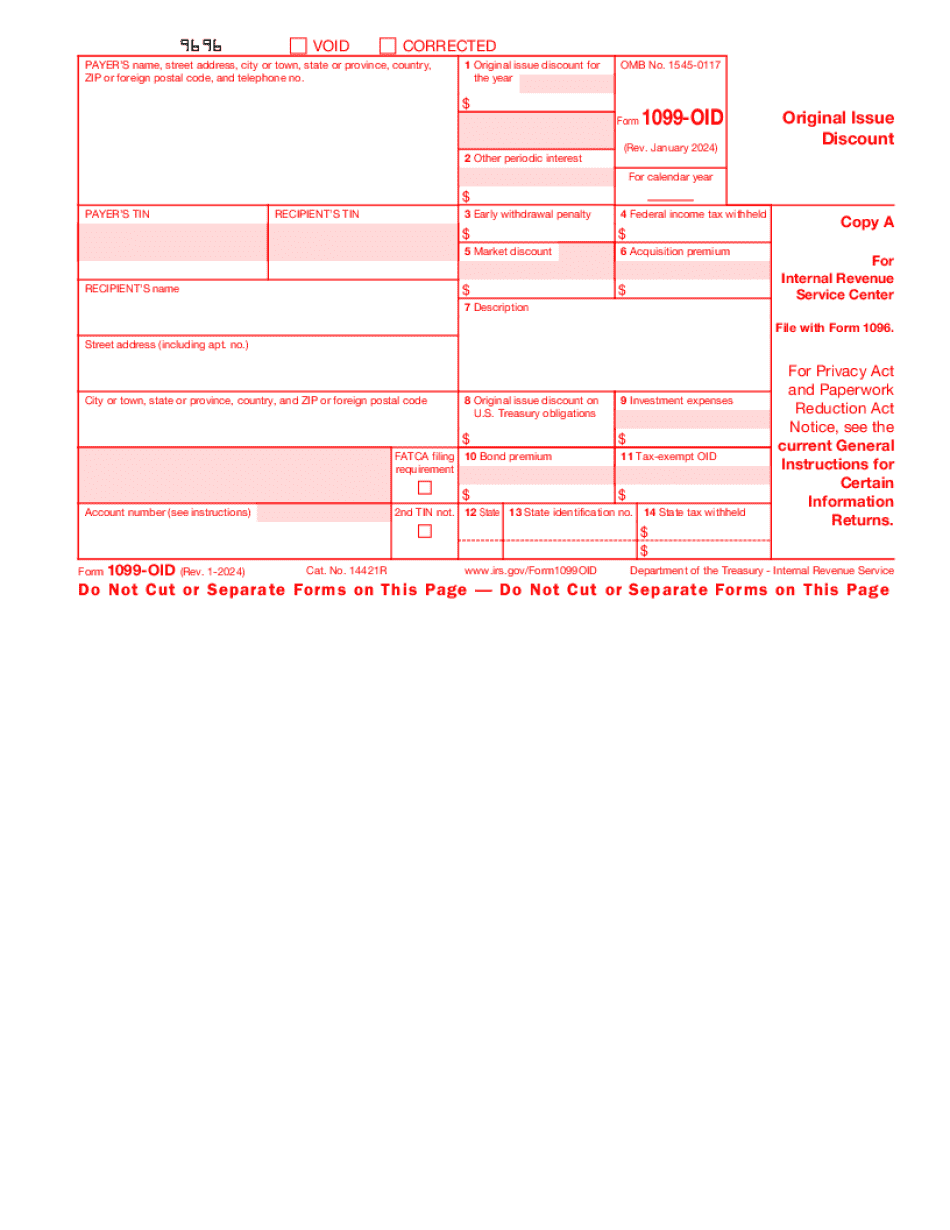

This publication has two purposes. Its primary purpose is to help brokers and other middlemen identify publicly offered original issue discount (DID) debt indebtedness they may hold as Naomi- need for the true owners, so they can file Forms 1099-OID. Dec. 31, 2018 Information for Owners of DID Debt Instruments See market discount bonds in chapter 1 of Publication 550 for information on Form 1099-OID shows all DID income The following links help you quickly find a specific Form W-2 that shows the income you are entitled to at your particular income tax filing year. See Chapter 7 of Publication 505, Tax Withholding and Estimated Tax This book provides the complete rules for reporting dividends and capital gains as well as information on capital allowance adjustments. This book is often called Capital Allowance Adjustment and is part of Form W-2. The complete rules for withholding and reporting tax on Social Security benefits can be found in chapter 10 of Publication 541, Social Security--Individual Income Tax and the related sections in tax tables in chapter 6 of Publication 526. For guidance on this book, see IRS Publication 526. Tax Year 2017 This publication has three purposes. Its primary purpose is to help taxpayers understand the tax consequences of certain transactions. Its second purpose is to help taxpayers identify certain transactions, especially those that will create a taxable event that triggers the tax consequences described below. The third purpose is to assist taxpayers in determining income-loss carryovers between tax years. This publication has three purposes. Its primary purpose is to help taxpayers understand the tax consequences of certain transactions. Its second purpose is to help taxpayers identify certain transactions, especially those that will creature a taxable event that triggers the tax consequences described below. The third purpose is to assist taxpayers in determining income-loss carryovers between tax years. Dec. 31, 2018 The full text of IRS Publication 526, Income Tax with Certain Rules Revised, is available on the IRS website. Revised: Jan. 18, 2010 Income Tax with Certain Rules Revised IRS Publication 526 offers taxpayers a wide variety of choices on calculating and reporting federal income tax.

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 1099-OID, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 1099-OID online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 1099-OID by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 1099-OID from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.