The 1098 mortgage interest statement is used to report interest of $600 or more that was paid on your mortgage within the previous tax year. The statement also itemizes amounts paid for private mortgage insurance during the year. We are required to mail out a 1098 to you on or before January 31st. You will receive a 1098 even if you've paid less than $600 in interest. A PDF copy will be available to download from your account at SLS net after January 31st. Let's take a closer look at the form. The top section contains the tax year, your account number, the primary borrower's name and mailing address, and the property address. If your mortgage was acquired by Specialized Loan Servicing after the beginning of the year, the beginning principal and escrow balance are transferred from your previous servicer. The principal section lists the beginning balance of the loan, the total amount that was paid towards the loan, and the ending balance for the tax year. The escrow section lists the beginning balance, the amount you paid into the account, the amount dispersed for taxes and insurance, and the ending escrow balance for the tax year. The interest paid section lists gross and net interest paid. The escrow disbursements section lists the taxes and insurance paid on the property and the mortgage insurance paid on the loan. The payment calculation section provides a breakdown of payment for the tax year, including principal and interest amounts per payment and total payment. The bottom section combines all of this information for you to include in your tax return. One report will show the total amount of home mortgage interest you paid, and another will report the total amount paid for your private mortgage insurance during the year. Important information related to certain states and mortgage insurance...

Award-winning PDF software

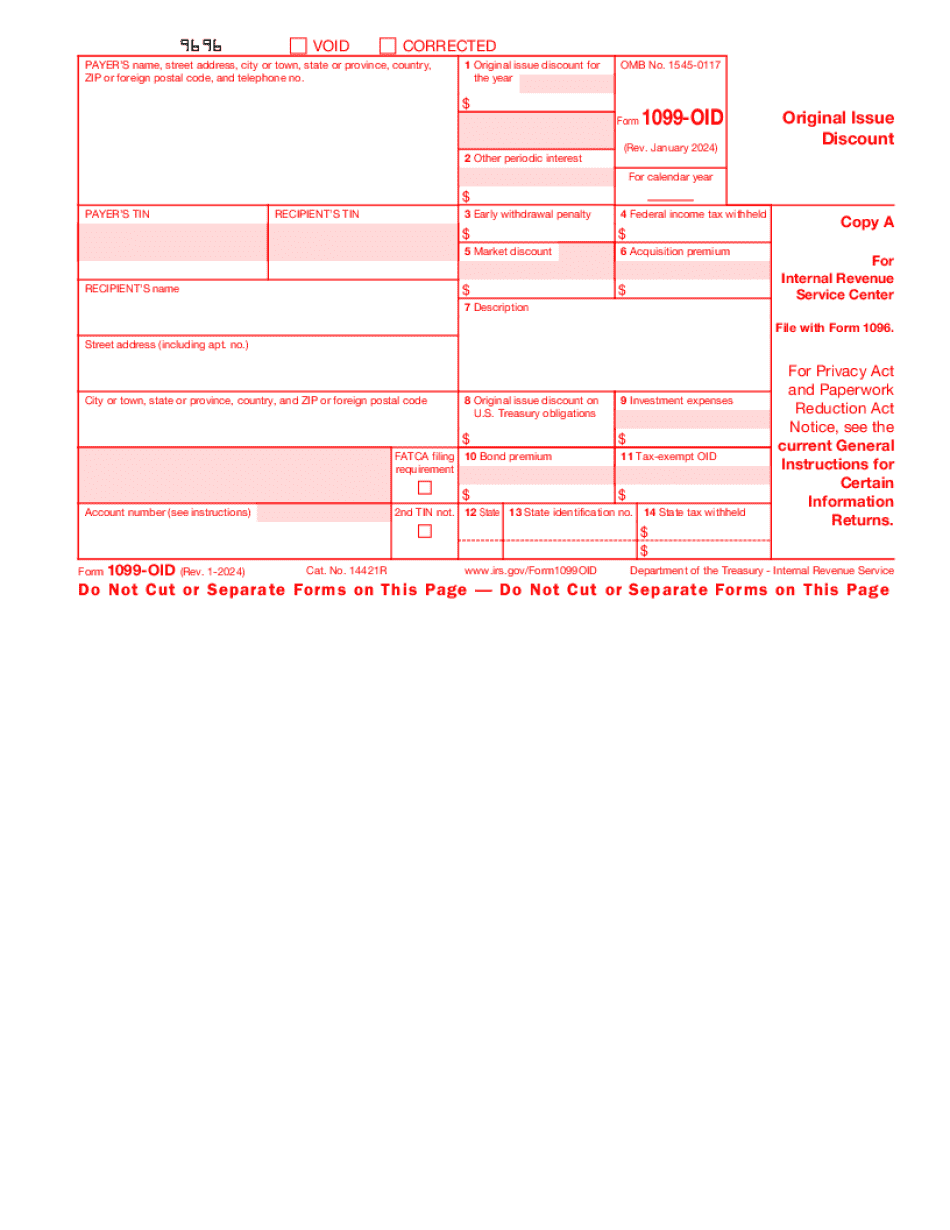

1099-int + mortgage interest Form: What You Should Know

Form 1099-INT: What It Is, Who Files It, and Who Receives It Key Takeaways · Form 1099-INT is an IRS income tax form used by taxpayers to report interest income received. · Brokerage firms, banks, mutual funds, and other How It Works and What to Do What Is 1099-INT? How It Works and What to Do Form 1099-INT: Interest Income — TurboT ax — Intuit Sep 25, 2025 — The IRS uses the information received from tax forms filed by individuals to determine whether those individuals have income.

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 1099-OID, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 1099-OID online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 1099-OID by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 1099-OID from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing 1099-int + mortgage interest